- Home

- About Us

- Become Self-Insured

- Alternative Security Program

- Injured Workers

- Knowledge Center

- Newsroom

|

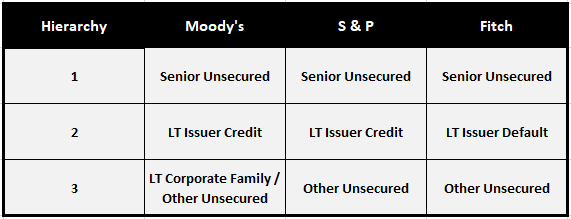

CREDIT RATINGS IN DEPTH For those wishing to more fully understand the details and fine points of the credit rating structure and how the Fund uses credit ratings, we provide the following information. Credit ratings (formal or implied) are utilized as a method to gauge the financial strength of Security Fund members while evaluating the potential risks that a member may pose in relation to all of the other members. A member's credit risk is used to price this risk into the Fund's assessment structure equitably. This risk pricing difference can be viewed on the assessment fee structure on the calculator page of this website. The Fund uses a numerical hierarchy in how it regards the different types of credit ratings that Moody's, Standard & Poor's and Fitch issue. Essentially, some kinds of credit ratings are a stronger indicator of credit strength and risk than others. The chart below lays out this hierarchy; for example, a rating that falls in the row for Hierarchy 1 is weighted more heavily than a rating in the row for Hierarchy 2 or 3.

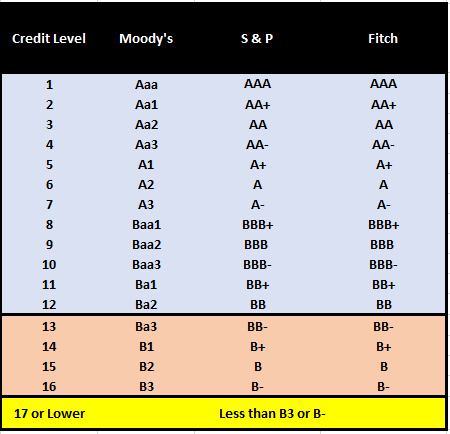

Split Credit Ratings Security Fund members may have formal credit ratings from multiple agencies at any given time. These multiple, and sometimes conflicting ratings are referred to as "split ratings." In these instances, the Fund has a policy in place to equitably and uniformly determine which rating shall be used for assessment. This policy ensures fairness, consistency, and predictability in the application of ratings. The Fund's policy is to use the most recent rating. If multiple ratings are issued on the same date, then the lowest published rating shall be used. Credit Rating Equivalency Between Different Rating Agencies The three credit rating agencies use different terminology for their ratings. The chart below shows the equivalency between the various rating agencies and relates these ratings to the Security Fund's credit level index.

Credit Rating Definitions Moody's Long-Term obligation ratings (e.g., Senior Unsecured, etc.): Moody's assigns ratings to long-term and short-term financial obligations. Long-term ratings are assigned to issuers or obligations with an original maturity of one year or more and reflect both on the likelihood of a default on contractually promised payments and the expected financial loss suffered in the event of default. Short-term ratings are assigned to obligations with an original maturity of thirteen months or less and reflect both on the likelihood of a default on contractually promised payments and the expected financial loss suffered in the event of default. Issuer Ratings (e.g., LT Issuer Credit, etc.) : Issuer Ratings are opinions of the ability of entities to honor senior unsecured debt and debt-like obligations. As such, Issuer Ratings incorporate any external support that is expected to apply to all current and future issuance of senior unsecured financial obligations and contracts, such as explicit support stemming from a guarantee of all senior unsecured financial obligations and contracts, and/or implicit support for issuers subject to joint default analysis (e.g. banks and government-related issuers). Issuer Ratings do not incorporate support arrangements, such as guarantees, that apply only to specific (but not to all) senior unsecured financial obligations and contracts. Corporate Family Rating: Moody's Corporate Family Ratings (CFRs) are long-term ratings that reflect the relative likelihood of a default on a corporate family's debt and debt-like obligations and the expected financial loss suffered in the event of default. A CFR is assigned to a corporate family as if it had a single class of debt and a single consolidated legal entity structure. CFRs are generally employed for speculative grade obligors but may also be assigned to investment grade obligors. The CFR normally applies to all affiliates under the management control of the entity to which it is assigned. For financial institutions or other complex entities, CFRs may also be assigned to an association or group where the group may not exercise full management control, but where strong intra-group support and cohesion among individual group members may warrant a rating for the group or association. A CFR does not reference an obligation or class of debt and thus does not reflect priority of claim. Source: Moody’s Standard & Poor's Issue Credit Ratings (e.g., Senior Unsecured, etc.): A Standard & Poor's issue credit rating is a forward-looking opinion about the creditworthiness of an obligor with respect to a specific financial obligation, a specific class of financial obligations, or a specific financial program (including ratings on medium-term note programs and commercial paper programs). It takes into consideration the creditworthiness of guarantors, insurers, or other forms of credit enhancement on the obligation and considers the currency in which the obligation is denominated. The opinion reflects Standard & Poor's view of the obligor's capacity and willingness to meet its financial commitments as they come due, and may assess terms, such as collateral security and subordination, which could affect ultimate payment in the event of default. Issuer Credit Ratings (e.g., LT Issuer Credit): A Standard & Poor's issuer credit rating is a forward-looking opinion about an obligor's overall creditworthiness. This opinion focuses on the obligor's capacity and willingness to meet its financial commitments as they come due. It does not apply to any specific financial obligation, as it does not consider the nature of and provisions of the obligation, its standing in bankruptcy or liquidation, statutory preferences, or the legality and enforceability of the obligation. Source: Standard & Poor’s Fitch Ratings Instrument Ratings (e.g., Senior Unsecured, etc.): The ratings of individual debt issues incorporate additional information on priority of payment and likely recovery in the event of default. The rating of an individual debt security can be above, below, or equal to the IDR, depending on the security's priority among claims, the amount of collateral, and other aspects of the capital structure. Issuer Default Rating (IDR) (e.g., LT Issuer Default, etc.): An Issuer Default Rating (IDR) is an assessment of an issuer's relative vulnerability to default on financial obligations and is intended to be comparable across industry groups and countries. Issuers may often carry both Long-Term and Short-Term IDRs. Because both types of IDRs are based on an issuer's fundamental credit characteristics, a relationship exists between them. Source: Fitch Ratings More Definitions Often, the issued ratings typically refer to specific obligations and not the company in general. Some of the primary classes of debt are: Senior Debt: Debt whose terms in the event of bankruptcy, require it to be repaid before subordinated debt receives any payment. Subordinated Debt: Debt over which senior debt takes priority. In the event of bankruptcy, subordinated debtholders receive payment only after senior debt claims are paid in full. Secured Debt: Debt that has first claim on specified assets in the event of default. Unsecured Debt: Debt that does not identify specific assets that the debt holder is entitled to in case of default. SEC – Office of Credit Ratings bulletin: The ABCs of Credit Ratings |